Starting on 6 April 2026 self-employed earners will become liable for Making Tax Digital (MTD) for the first time. HMRC is implementing Making Tax Digital to overhaul the self-assessment tax reporting system. Phase 1 begins at the start of the next tax year on 6 April 2026.

Are You Ready for the Rollout of Making Tax Digital in April 2026?

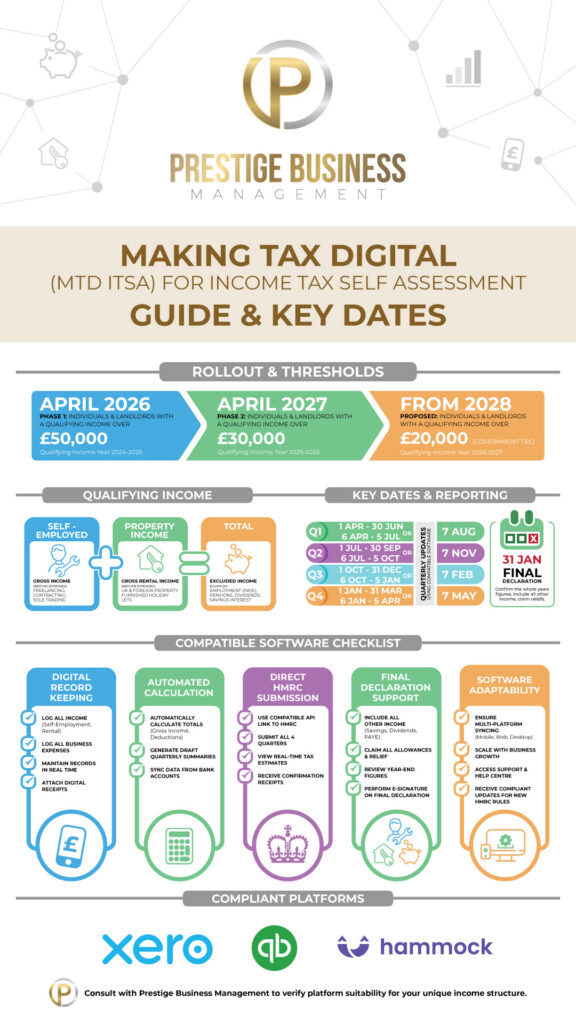

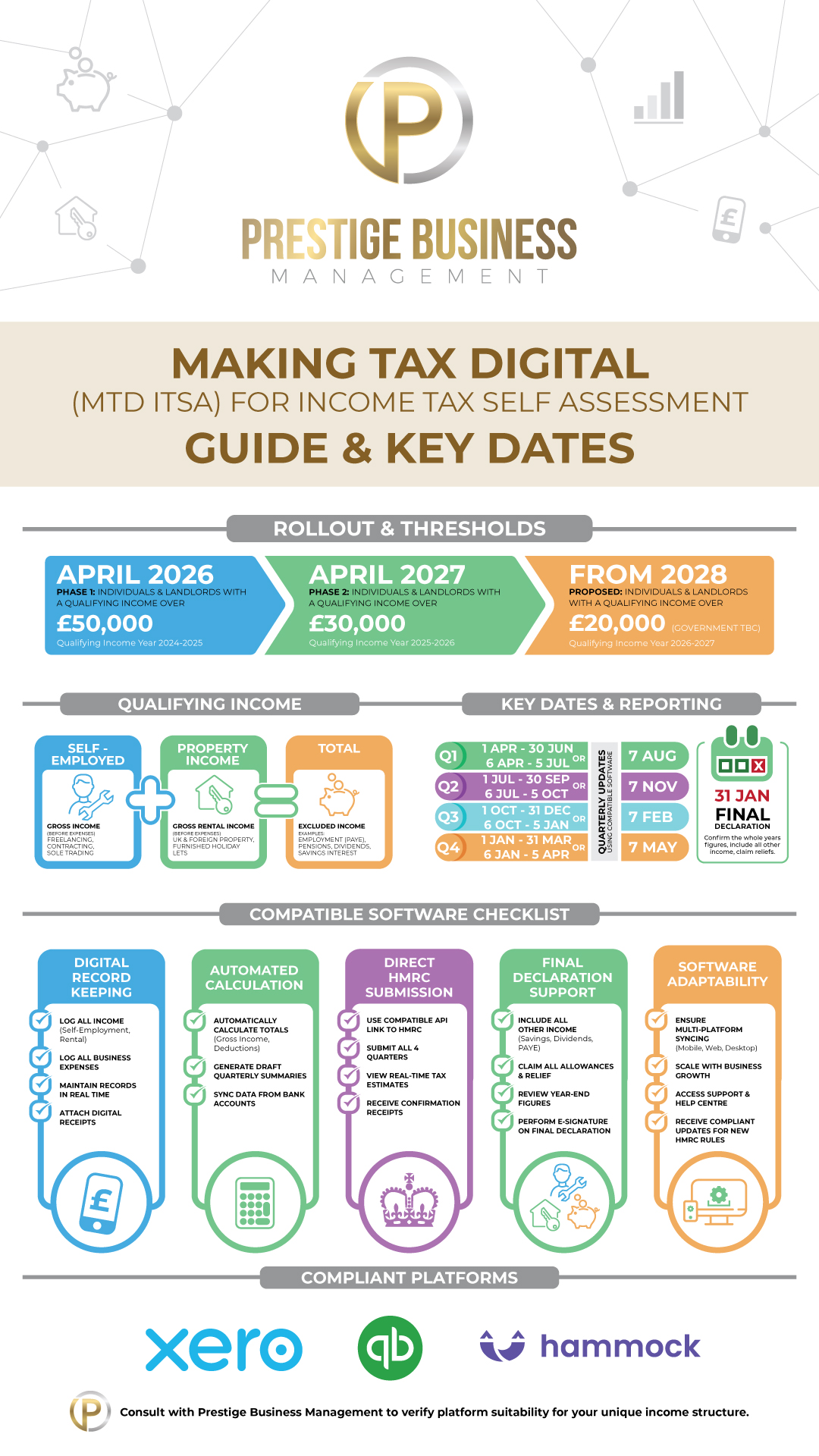

The scheme requires tax to be filed digitally, using compatible software, as well as submitting quarterly updates to HMRC. This replaces the traditional annual self-assessment process and becomes mandatory for all those submitting via self-assessment over the next three years. Those earning over £50,000 annually will be required to file under Making Tax Digital from April 2026. Here we explain what you need to do and when Making Tax Digital applies to you.

What is Making Tax Digital?

What is Making Tax Digital?

Making Tax Digital is a scheme under which self-employed individuals and landlords will be required (mandated) to submit digital records and provide quarterly updates on their income and expenditure to HMRC using software that is compatible with the Making Tax Digital system.

Who Does Making Tax Digital Apply to?

Those with an annual, qualifying income of over £50,000 must start filing under Making Tax Digital from 6 April 2026. Those with a qualifying income between £30,000 and up to £50,000 per year will need to comply with MTD from April 2027. Those earning £20,000 or more annually will become liable to report under Making Tax Digital from April 2028. Qualifying income is your total gross income, before expenses, from specified sources. If you have multiple sources of income, you must add them together to get your total gross income.

Qualifying income, what’s included:

-

- Self-Employment: All turnover from sole trader businesses, freelancing

- Property Income: Total rental income from UK and overseas properties, which includes Furnished Holiday Lets (FHLs)

Excluded (Does not count towards the qualifying income threshold)

-

- Employment income (PAYE)

- Savings interest and dividends

- State or private pensions

- Partnership income (currently out of scope)

The government has abandoned plans to extend Making Tax Digital to corporation tax. HMRC has confirmed that MTD for corporation tax will not proceed due to the complexity of corporation tax, making it difficult to apply the required digital recordkeeping and updates to the breadth of businesses that owe corporation tax.

Why Are HMRC Making Tax Digital?

The majority of customers want to get their tax right, yet the tax gap is estimated at 5.3% of total theoretical tax liabilities, or £46.8 billion, for the tax year 2023 to 2024. Making Tax Digital aims to reduce errors, improve accuracy and transparency, and provide a clearer, more up-to-date picture of finances. HMRC hopes the scheme will alleviate the pressure of the tax rush to calculate and submit in January and create a more manageable routine throughout the year for those submitting tax records via self-assessment. They believe that, over time, Making Tax Digital will benefit the economy by reducing the administrative burden of filing taxes, thereby increasing productivity and revenue. There can be other benefits to digitising the tax process, including the improved accuracy that digital records provide and the help and guidance built into many software products.

What You Need to Know

You need to know from what date to start filing under Making Tax Digital. Mandatory registration depends on your “qualifying income” from the previous tax year:

| Phase | Start Date | Qualifying Income Threshold | Based on the Tax Year |

| Phase 1 | 6 April 2026 | Over £50,000 | 2024–25 |

| Phase 2 | 6 April 2027 | Over £30,000 | 2025–26 |

| Phase 3 | 6 April 2028 | £20,000 or more | 2026–27 |

Making Tax Digital requires you to submit quarterly updates and a final declaration by 31 January the following year.

Key Filing Dates:

| Reporting Period | Update Period | Submission Deadline |

| Quarter 1 | 6 April – 5 July | 7 August |

| Quarter 2 | 6 July – 5 October | 7 November |

| Quarter 3 | 6 October – 5 January | 7 February |

| Quarter 4 | 6 January – 5 April | 7 May |

| Final Declaration | Full Tax Year | 31 January (following year) |

Good to Know

For the first year (2026/27), HMRC is operating a “soft landing” where no penalty points will be issued for late quarterly updates. Following this soft landing period, penalties will apply if you repeatedly miss deadlines. The idea is to encourage on-time filing using a new points-based penalty system that penalises persistently late filers, rather than occasional errors. An exemption exists for the digitally excluded, which applies to those who do not use computers for religious reasons and those who are unable to comply because of age, disability or location (or for any other justifiable reason). Each case would need to be decided on its merits. Location covers those who cannot access broadband due to where they live. The exemption will not apply to those who could sign up for broadband but have not done so. HMRC has issued guidance about how to apply for a digital exclusion exemption.

Prestige Business Management Works for You

Prestige Business Management can support you with starting Making Tax Digital. We provide full training to all our clients on how to use the best business management platforms, such as QuickBooks and Xero. Further to this, you can automate the scanning of invoices, bills, and receipts with Dext. For landlords, we have partnered with property specialists Hammock to support our clients with making Tax Digital. Or we can offer simple spreadsheet solutions, depending on how you prefer to work. Find out what we can do for you. Call us today on 0203 773 2927.