Everyone can appreciate good record keeping. Especially your accountant, plus it could save you lots of time when you come to file your tax return and save you money on your tax bill if you keep a tax record in good order. Good record keeping is also helpful if HM Revenue and Customs (HMRC) wants to ask any questions. Here we outline what you need to do to keep a tax record, depending on your business model.

How to Keep a Tax Record

If you are a start-up, make sure you keep a tax record in good order right from the start. Embedding good record keeping into your daily running processes will help you maintain good records and efficiency moving forwards and will help keep you compliant. You should be keeping a record of all documents that you have received, or copies of those which you have prepared. These records will be from the accounting period or tax year to which they relate, or sometimes soon afterwards. Prestige Business Management can guide you through the tax return process and provide automated accounts in a format of your choice, depending on how you like to work. We provide full training to all our clients on how to use the best business management platforms like QuickBooks. Further to this you can automate scanning invoices, bills and receipts with apps that we are partnered with including Dext, formerly Receipt Bank.

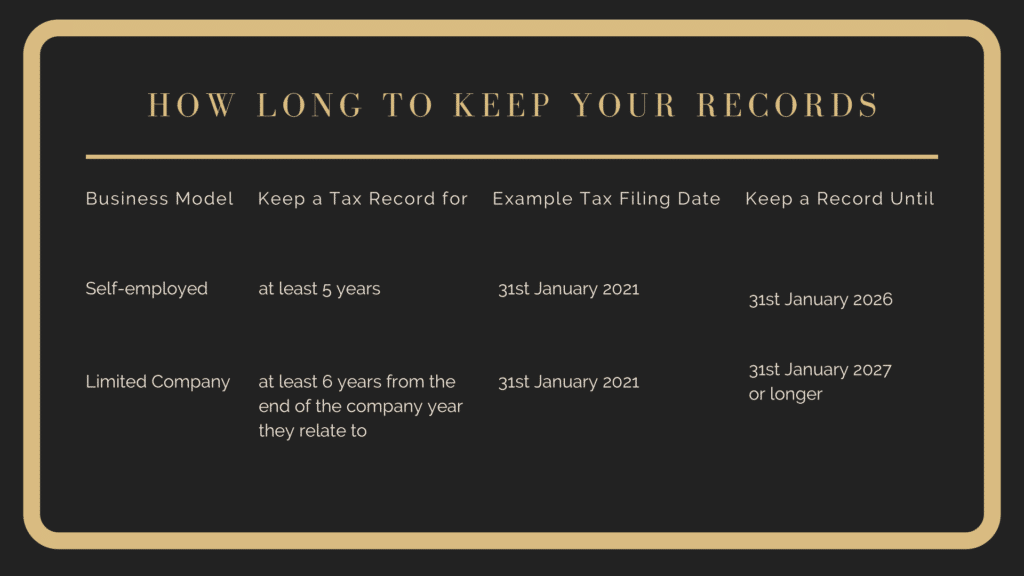

How Long You Should Keep Documents for a Tax Record

If you are self-employed, or in a partnership, you need to keep a tax record for at least five years from 31 January following the tax year that the tax return relates to. You will need to keep a tax record for longer if you have filed your tax return late, or if HMRC has started a check on your return, or if you’re buying and selling assets. A limited company needs to keep a tax record for six years after the end of an accounting period. There are some situations when limited companies need to keep records for longer. If you file your tax return late, or it is subject to a compliance check, then the amount of time you need to keep a tax record may be extended. This applies to any organisation that falls within the charge to corporation tax, including members’ clubs, societies and associations. Individuals not carrying on a business need to keep a tax record for 22 months following the end of the tax year they relate to. An individual also includes the trustee of a settlement and the personal representative of a deceased person. If HMRC requests to check your tax return for any reason but you are unable to present the records that you used to complete the return, it’s possible you may have to pay a penalty. Sometimes you may need to refer to records that are several years old. For example, if you dispose of an asset, such as land, shares or a valuable chattel, that you have owned for a long time. A chattel is the tangible personal property that is movable between locations. It can refer to either animate or inanimate property such as livestock, antique furniture or vehicles. You may need to have older records to calculate a capital gain or loss. Plus there are some other circumstances that may cause you to need to refer to older records. Our business finance specialists can advise you about what assets relate to capital gains and how to fulfil older tax record information.

Making Tax Digital

HMRC has introduced legislation called Making Tax Digital in order to avoid mistakes, which can cost both your business and the Exchequer. The majority of customers want to keep a tax record correctly and get their tax right, however tax gap figures indicate that a large number of avoidable mistakes is costing an estimated £35 billion, which is 5.3% of tax liabilities for the year, which were £674 billion. The improved accuracy that digital records provide, along with the help built into many software products and the fact that information is sent directly to HMRC from the digital records, avoiding transposition errors, will reduce the amount of tax lost to avoidable errors. VAT-registered businesses with a taxable turnover above the VAT threshold (£85,000) are now required to follow the Making Tax Digital rules by keeping digital records and using software to submit VAT returns. VAT-registered businesses with a taxable turnover below £85,000 will be required to follow Making Tax digital rules for their first return starting on or after April 2022. If you are below the VAT threshold you can voluntarily join the Making Tax Digital service now. Self-employed businesses and landlords with annual business or property income above £10,000 will need to follow the rules for MTD for Income Tax from their next accounting period starting on or after 6 April 2023. The government will provide businesses with an opportunity to take part in a pilot for Making Tax Digital for Corporation Tax and will not mandate its usage before 2026. All existing Prestige Business Management clients are already set up for MTD. Our processes are MTD compliant in partnership with Quickbooks and other cloud accounting software, suitable to our clients needs.

What You Need to Keep a Tax Record

What you need to keep a tax record will depend on the number and complexity of the claims you make, according to your business model. If you are a start-up check out our Guide to Self-Employed Versus Limited Company.

Self-Employed

You’ll need to keep records of:

- all sales and income

- all business expenses

- VAT records if you’re registered for VAT

- PAYE records if you employ people

- records about your personal income

- your grant, if you claimed through the Self-Employment Income Support Scheme because of coronavirus

You do not need to submit when you file your tax return but you need to keep them so you can:

- work out your profit or loss for your tax return

- show them to HMRC if asked

You must make sure your records are accurate and keep proof

Types of proof include:

- all receipts for goods and stock

- bank statements, cheque book stubs

- sales invoices, till rolls and bank slips

Record Allowable Expenses

If you’ve had to pay for things like tools for work, travel costs or specialist clothing for work, you may be able to claim for these to reduce the tax you’ll have to pay. You need to keep a record of these so you can include them in your tax return.

Top Tips

Our business finance specialists recommend that you set-up a separate bank account to help divide your own personal money from your day-to-day business account needs. Reconcile your accounts regularly, at least once a month. Your income and expenditure records need to match up with your financial statements. So spend time creating and maintaining your filing system – you can break down your paperwork by year, quarter or month, depending on what works for your business. The important thing is to stay on top of your filing. Prestige Business Management can help set-up or streamline your business processes and recommend management tools and platforms to help you keep a tax record.

Employees and Limited Company Directors

You need to keep documents about your pay and tax, including:

- P45 – if you leave your job, this shows your pay and tax to the date you left

- P60 – if you’re in a job on 5 April, this shows your pay and tax for the tax year

- P11D – this shows your expenses and benefits

- certificates for any Taxed Award Schemes

- information about any redundancy or termination payment

Contact your employer if you do not have your P60, P45 or form P11D.

Submit Allowable Expenses

You need to record any extra costs that you incur as part of your work. The cost of these should be claimed directly from the company. Each company will have a process for claiming expenses, be it a flat rate per mile for travelling by car or a per diem, which is the term used for a daily allowance. This is a specific amount of money that an organisation gives an individual, typically an employee, per day to cover living expenses when travelling on the employer’s business. For your expenses to qualify for reimbursement, you will need to supply a valid receipt or invoice for the cost, including a VAT number where applicable, the date and time must also match the cost incurred. Most employers accept photo images of expenses receipts now. Make sure all of this information is clearly visible and only attach the relevant receipts to the expense claim.

Benefits records

Keep any documents relating to these:

- social security benefits

- Statutory Sick Pay

- Statutory Maternity, Paternity or Adoption Pay

- Jobseeker’s Allowance

Employee Share Schemes or Share-related Benefits

You should keep:

- copies of share option certificates and exercise notices

- letters about any changes to your options

- information about what you paid for your shares and the relevant dates

- details of any benefits you’ve received as an employee shareholder

Savings, Investments and Pensions

You should keep:

- bank or building society statements and passbooks

- statements of interest and income from your savings and investments

- tax deduction certificates from your bank

- dividend vouchers you get from UK companies

- unit trust tax vouchers

- documents that show the profits you’ve made from life insurance policies (called ‘chargeable event certificates’)

- details of income you get from a trust

- details of any out-of-the ordinary income you’ve received, like an inheritance

Pension

You should keep:

- P160 (Part 1A) which you got when your pension started

- P60 which your pension provider sends you every year

- any other details of a pension / State Pension and the tax deducted from it

Rental Income

Keep details of:

- dates when you let out your property

- all rent you get

- any income from services you give to tenants (for example if you charge for maintenance or repairs)

- rent books, receipts, invoices and bank statements

- allowable expenses you pay to run your property (for example services you pay for such as cleaning or gardening)

Capital Gains

You need to keep records about your capital gains for at least a year after the Self Assessment deadline. Businesses must keep records for 5 years after the deadline.

Keep receipts, bills and invoices that show the date and the amount:

- paid for an asset

- additional costs like fees for professional advice, Stamp Duty, improvement costs, or to establish the market value

- received for the asset – including things like payments you get later in instalments, or compensation if the asset was damaged

Keep any contracts for buying and selling the asset (for example from solicitors or stockbrokers) and copies of any valuations.

Overseas income

You should keep:

- evidence of income you’ve earned from overseas, like payslips, bank statements or payment confirmations

- receipts for any overseas expenses you want to claim to reduce your tax bill

- dividend certificates from overseas companies

- certificates or other proof of the tax you’ve already paid – either in the UK or overseas

Small Businesses

You need to keep:

- sales and income

- self-employed expenses

- VAT records (if you’re VAT registered)

- PAYE records if you have employees

- details of personal income (for example from savings, investments and rental income)

- coronavirus grant details

Keep proof alongside your records, including all receipts (for goods, stock, and expenses), bank statements, cheque stubs, sales invoices, purchase orders, till rolls and bank slips.

Prestige Business Management has a suite of products and services to help you keep a tax record and automate filing systems with the latest technology and fintech platforms.

Limited Companies

The main difference between a limited company and self-employment, is that a limited company is a separate entity in its own right. This means you need to keep records of the company itself (not just financial records). These include:

- directors, shareholders and company secretaries

- shareholder votes and resolutions

- debentures (promises to repay a loan at a future date)

- indemnities (payments to make when things go wrong and it’s the company’s fault)

- transactions when people buy shares

- loans and mortgages secured against the company’s assets

You should also have a register of ‘people with significant control’ (PSCs). PSCs are likely to be people who have:

- more than 25% of shares in the company

- more than 25% of voting rights in the company

- the right to appoint or remove the majority of the board of directors

If you don’t keep your records in the same place as your registered address, you need to tell Companies House.

If you are found to be lacking in accounting records, you can be fined £3,000 and disqualified as a company director, so it’s important you do this correctly. As well as information about the company, you need to keep financial and accounting records:

- money spent and received by the company

- details of assets owned

- details of debts the company owes or is owed

- stock the company owns at the end of the financial year

- stocktakings used to work out that figure

- all goods bought and sold (and who from and to)

You should have all the records needed to file your company tax return, including:

- turnover

- income (including profits, trading losses brought forward, property income)

- chargeable gains

- profits before other deductions and reliefs

- deductions and reliefs

- tax reliefs and reductions

- tax reconciliation

- losses

At Prestige Business Management we can help your Business

It’s important to take sound financial advice. Contact Prestige Business Management for targeted guidance and information on anything in this guide. We are here to help and we pride ourselves on our communication and our straightforward guidance for start-ups and tailoring the most effective accounting for your business, for every stage of growth. Find out what we can do for you. Call us today on 0203 773 2927.