The Construction Industry Scheme (CIS) VAT reverse charge will come into force on 1st March 2021. The CIS VAT reverse charge was due to commence in October 2019, but this was delayed twice, firstly as a result of Brexit and then the outbreak of COVID-19.

The construction industry reversed charge will apply to supplies of construction work in the UK. When the reverse charge applies the customer accounts for the supplier’s output VAT. This measure only applies to construction supplies made by a business to business.

What the CIS VAT reverse charge means, is that the customer receiving the service will have to pay the VAT due to HMRC instead of paying it to the supplier.

It will only apply to individuals or businesses registered for VAT in the UK.

The reverse charge will affect supplies of building and construction services supplied at the standard or reduced rates that also need to be reported under CIS. These are called specified supplies.

There is an important difference between CIS and the reverse charge where materials are included within a service. The reverse charge applies to the whole service whereas CIS payments to net status sub-contractors are apportioned and no deductions are made on the materials content.

How to Prepare for the Construction Industry Reverse Charge

- make sure your accounting systems and software can deal with the reverse charge

- consider whether the change will impact your cash flow

- make sure all your staff who are responsible for VAT accounting are familiar with the reverse charge and how it will work

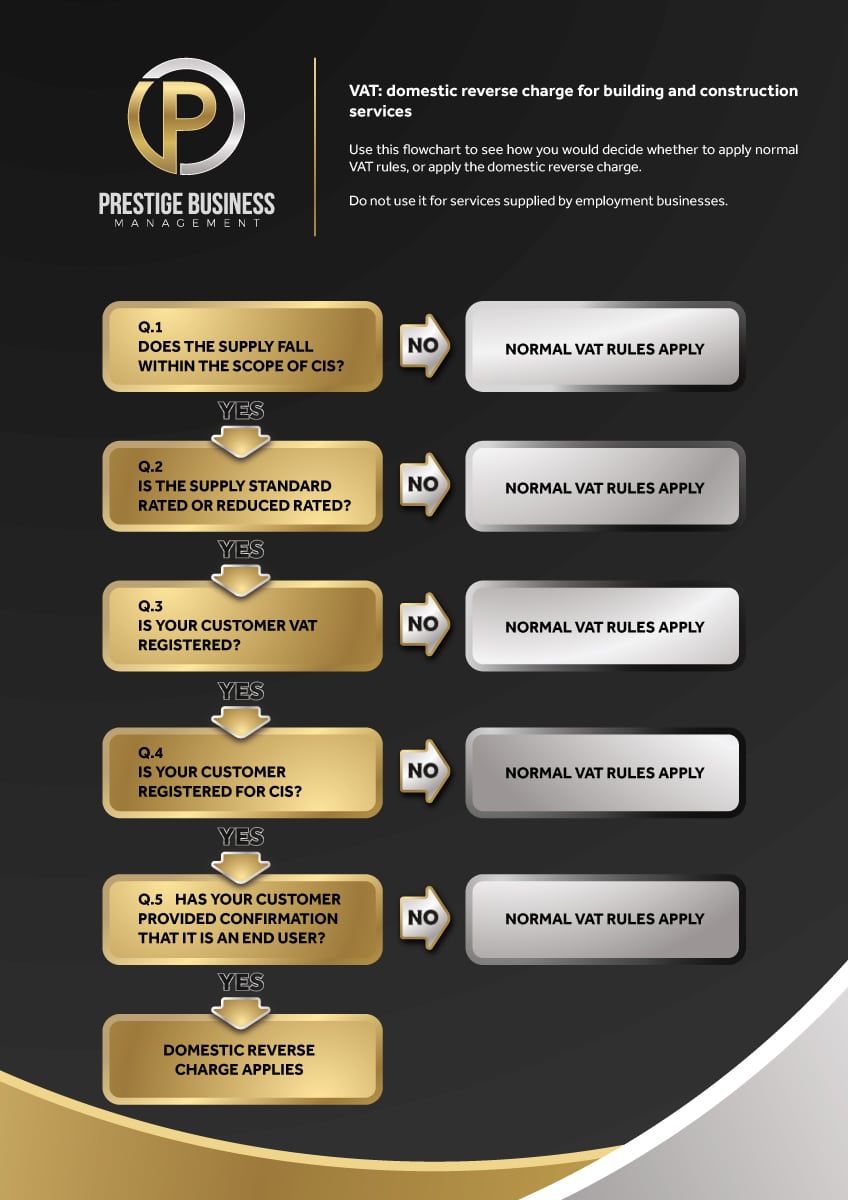

If the VAT reverse charge does not apply you should follow the normal VAT rules. The government has provided flow charts to help you decide if you need to use the reverse charge, which you can view and download here.

When you Must use the CIS VAT Reverse Charge

You must use the reverse charge for the following services:

Constructing, altering, repairing, extending, demolition or dismantling buildings or structures (whether permanent or not), including offshore installation services, constructing, altering, repairing, extending, demolishing of any works forming, or planned to form, part of the land, including (in particular) walls, roadworks, power lines, electronic communications equipment, aircraft runways, railways, inland waterways, docks and harbours, pipelines, reservoirs, water mains, wells, sewers, industrial plant and installations for purposes of land drainage, coast protection or defence.

Installing heating, lighting, air-conditioning, ventilation, power supply, drainage, sanitation, water supply or fire protection systems in any building or structure internal cleaning of buildings and structures, so far as carried out in the course of their construction, alteration, repair, extension or restoration painting or decorating the inside or the external surfaces of any building or structure services which form an integral part of, or are part of the preparation or completion of the services described above – including site clearance, earth-moving, excavation, tunnelling and boring, laying of foundations, erection of scaffolding, site restoration, landscaping and the provision of roadways and other access works.

When Not to use the CIS VAT Reverse Charge

Do not use the charge for the following services, when supplied on their own:

Drilling for, or extracting, oil or natural gas, extracting minerals (using underground or surface working) and tunnelling, boring, or construction of underground works, for this purpose manufacturing building or engineering components or equipment, materials, plant or machinery, or delivering any of these to site manufacturing components for heating, lighting, air-conditioning, ventilation, power supply, drainage, sanitation, water supply or fire protection systems, or delivering any of these to site.

The professional work of architects or surveyors, or of building, engineering, interior or exterior decoration and landscape consultants making, installing and repairing art works such as sculptures, murals and other items that are purely artistic signwriting and erecting, installing and repairing signboards and advertisements installing seating, blinds and shutters installing security systems, including burglar alarms, closed circuit television and public address systems.

Read the full Government Guidance here.

Cash Flow

Now the VAT reverse charge might have some significant changes to your businesses cash flow and this will have to be considered as you can see in the example below. The flat rate VAT scheme and VAT cash basis scheme might not work in your favour anymore. For larger subcontractors switching to monthly VAT return filings might make more sense under the VAT reverse charge scheme. We are happy to advise you further on this and HMRC has highlighted it here.

Examples of CIS & VAT Reverse Charge

Jane hires Pinnacle Properties Ltd for some work on her house, which makes Jane the end customer.

Pinnacle Properties Ltd hires Dave the electrician as a subcontractor to complete the electrical works at Jane’s house. Pinnicale Properties and Dave are both CIS and VAT registered.

Dave completes the electrical work and invoices £1000 for his labour and here is where the reverse charge will take effect:

| Before Reverse Charge | After Reverse Charge |

| Labour: £1,000 | Labour: £1,000 |

| Materials: £100 | Materials: £100 |

| Sub Total: £1,100 | Sub Total: £1,100 |

| VAT: £220 | VAT: £0 |

| CIS (labour only): -£200 | CIS (labour only): -£200 |

| Total £1,120 | Total £900 |

Pinnacle Properties will then invoice Jane for all of the works they have carried out including the work Dave did. In this example let’s say that is for £10,000.

| Before Reverse Charge | After Reverse Charge |

| Labour & Materials: £10,000 | Labour & Materials: £10,000 |

| VAT: £2000 | VAT: £2,000 |

| Total £12,000 | Total £12,000 |

As you can see there is no difference for Pinnacle Properties in how they will Invoice Jane as she is the end user and normal VAT rules apply. But now lets say Pinnacle Properties was hired by another company CJ Property Ltd who is also CIS and VAT registered and Jane hired CJ Property to carry out the work. This will not change how Dave invoices Pinnacle, that will remain the same. So now Dave is invoicing Pinnacle, who is invoicing CJ who in return will invoice Jane the end user.

Pinnacle Properties invoice to CJ Property will be as follows.

| Before Reverse Charge | After Reverse Charge |

| Labour: £8,000 | Labour: £8,000 |

| Materials: £2,000 | Materials: £2,000 |

| Sub Total: £10,000 | Sub Total: £10,000 |

| VAT: £2,000 | VAT: £0 |

| CIS (labour only): -£1,333.33 | CIS (labour only): -£1,333.33 |

| Total £10,666.67 | Total £8,666.67 |

CJ Property Ltd will now invoice Jane as normal and include VAT on their invoice, the same as Pinnacle did when they invoiced Jane in the above example.

In this flowchart you can see when normal VAT rules will apply and when the VAT Reverse Charge applies. Click here to download your copy: PBM – VAT CIS RC FLOW CHART

PBM VAT CIS Flow Chart

At Prestige Business Management we can help your Business

At Prestige Business Management we can help your business understand the best solutions for the success of your business. Find out what we can do for you. Call us today on 0203 773 2927.